You filed your return. You paid what you owed. You waited three years and assumed that chapter of your life was closed for good. But what if that window never actually closed?

Under a little-known interpretation of the “fraud exception” to the statute of limitations, misconduct by your tax preparer—not you—can keep an IRS audit window open indefinitely. In many courts, it doesn’t matter if you never intended to cheat or never even knew anything was wrong. Because you signed that return, the preparer’s fraud can be imputed to you.

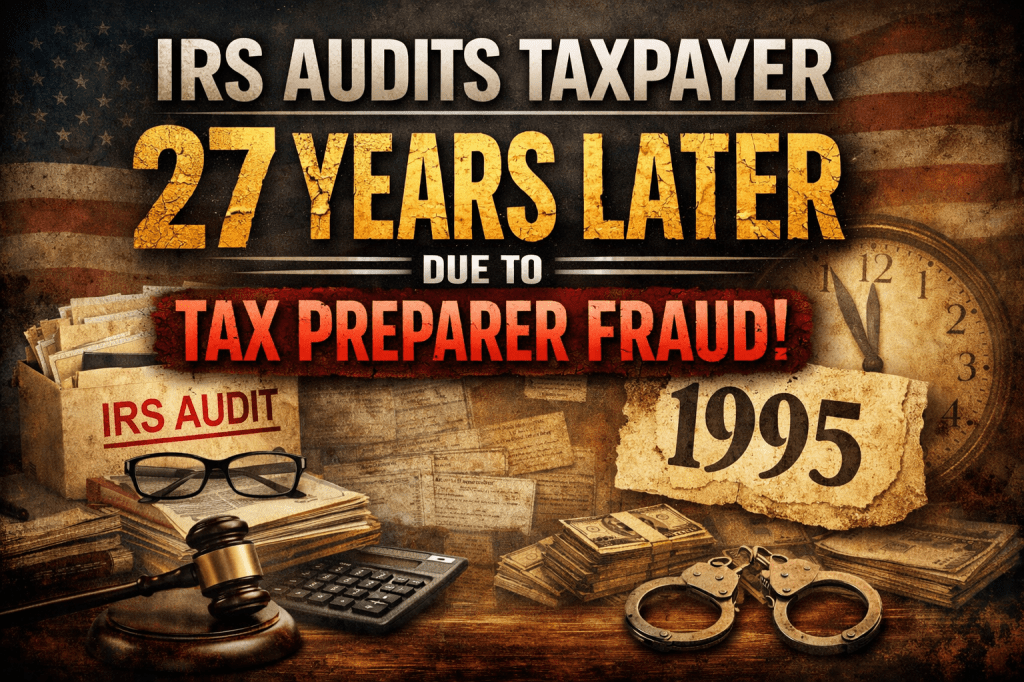

The IRS Knocks—27 Years Later!

Consider the recent case of Murrin v. Commissioner. Stephanie Murrin, a New Jersey resident, filed her 1993–1999 tax returns on time. There was no evidence that she personally intended to evade taxes. However, her preparer, Duane Howell, inserted false items on those returns to understate her tax liability. Howell eventually pled guilty to federal tax fraud in 2007—all without Murrin’s knowledge.

Fast-forward to 2019: Twenty-seven years after those returns were filed, the IRS issued a notice of deficiency. Relying on the fraud exception in Section 6501(c)(1), the IRS bypassed the normal three-year statute of limitations. They asserted that Murrin owed:

- $65,000 in back taxes

- $13,000 in penalties

- Over $250,000 in interest

The government’s position was simple: because the returns were fraudulent (even if the fraud was the preparer’s), the assessment period never closed.

Why “I Didn’t Know” Is Not a Defense

In October 2025, the U.S. Court of Appeals for the Third Circuit affirmed that fraud by a preparer is enough to trigger an unlimited audit window. This follows previous rulings like Allen, Magill, and Kooyers, which emphasize that the taxpayer—not the preparer—has the ultimate responsibility to file a correct return.

In the eyes of the Tax Court, delegating the preparation of your taxes does not delegate your legal responsibility. Ignorance is not a defense.

How to Protect Yourself

To keep decades-old tax returns from coming back to life, you need to be proactive. Here are five ways to protect your future:

- Read Your Return Like an Auditor: Compare every line to your W-2s, 1099s, and K-1s. Challenge any “strategy” or deduction you can’t support with paper. If a deduction looks too good to be true, it probably is.

- Keep a Long Paper Trail: Since the three-year rule can vanish in fraud cases, you may need to prove your good faith decades later. Keep digital copies of filed returns, workpapers, and emails with your preparer indefinitely.

- Be Wary of “Fraud” Language in Agreements: Never sign a stipulation or settlement saying your return was “fraudulent” without understanding the impact. Once fraud is admitted, a 75% civil fraud penalty can attach, and it is nearly impossible to unwind.

- Fix Problems Quickly: If you find a mistake, amend and pay as soon as possible. This won’t erase existing fraud, but it shows you aren’t trying to keep an improper benefit and can reduce ongoing interest.

- Be Deliberate About Where You Litigate: If the IRS comes knocking on a “forever” audit, the choice of court matters. The Tax Court often rules against the taxpayer in these scenarios, while other courts focus more on the taxpayer’s personal intent. Strategic selection of your legal forum is vital.

The Takeaway

At Howard Tax Prep LLC, we always say: We fix tax problems. But the best way to fix a problem is to prevent it. You are legally responsible for every number on your return. Don’t let a dishonest preparer turn your “three-year window” into a “forever” nightmare.

Is your current preparer giving you answers you can’t support? It might be time for a second opinion.